As global digitalization enters a new phase where “computing power equals productivity”, data centers are no longer mere “digital warehouses” but have evolved into the “second power grid” that determines the competitiveness of nations and enterprises. In 2025, at the convergence of four transformative forces—generative AI, 5G-Advanced, sustainable finance, and regulatory sandboxes—Artificial Intelligence Data Centers (AIDC) achieved the unprecedented capability of “self-iteration, self-optimization, and self-profitability” for the first time. They transitioned from cost centers to value hubs, thereby redefining the business logic and industrial boundaries across thousands of sectors including telecommunications, internet services, manufacturing, healthcare, and finance.

From “Resource Pools” to “Intelligent Entities”: The Paradigm Shift in AIDC Technology

Chips – A “Moonshot Leap” in Computing Density

NVIDIA’s Blackwell Ultra, mass-produced in late 2025, boosted FP4 inference performance by 1.5 times. Its 2026 Vera Rubin platform further tripled performance, pushing single-cabinet power consumption to 600 kW. Google’s Willow quantum chip delivered a 13,000-fold advantage in specific algorithms, making “quantum-classical hybrid computing” a new standard for supercomputing centers. With three types of heterogeneous computing power—GPU, ASIC, and QPU—coexisting in one cabinet, traditional air cooling proved inadequate for heat dissipation. This drove the full-scale adoption of liquid cooling solutions at cabinet, board, and even wafer levels: Microsoft’s microfluidic channels reduced GPU temperatures by 65% and tripled the energy efficiency ratio of data centers.

Networks – From “North-South Traffic” to “East-West Traffic” and Beyond to “Intra-Cluster Traffic”

Large model training generates 30% intra-machine All-Reduce traffic, propelling switch chips into the 51.2 T era. Co-Packaged Optics (CPO) shortened SerDes distances to 5 mm and cut power consumption by 40%, laying the groundwork for “GPU pooling”. By 2025, mainstream AIDCs had adopted the concept of “computing clusters”—each unit scheduled with 256 GPUs, boasting network latency < 2 µs and packet loss rate < 10⁻⁶, forming a new topology where “a cabinet functions as a computer”.

Storage – From “Hot-Cold Tiering” to “Training-Grade All-Flash”

The peak write speed of large model checkpoints reached 2 TB/s, a load that traditional SAS drives could not handle efficiently without causing GPU bottlenecks. In 2025, the integration of PCIe 5.0 NVMe and CXL 3.0 gave rise to “memory pools with integrated storage, computing, and switching”. A baseline configuration of 8 TB memory and 200 Gbps bandwidth per node improved training efficiency by 18%–24%.

Energy – From “Dual Carbon Compliance” to “Zero-Carbon Profitability”

For AI workloads, every 0.1 reduction in PUE translated to annual electricity savings of 32 million yuan for a 10,000-GPU cluster. In 2025, AIDCs turned “energy management” into a standalone P&L line: dynamic power capping, second-life battery utilization, and waste heat recovery from liquid cooling systems (with 45°C inlet water and 60°C outlet water) were used to heat nearby office buildings, generating 8 million yuan in annual revenue per data center. Combined with green power futures and carbon credit trading, 12% of EBIT for some AIDCs came directly from zero-carbon operations.

Three Leaps in Business Models: From Cabinet Rental to Outcome Selling

Leap 1: IaaS → MLaaS (Machine Learning as a Service)

In 2025, mainstream customers no longer rented “x86+GPU” hardware; instead, they subscribed directly to “1 PFLOPS computing power packages” that included data cleaning, model distillation, inference optimization, and API gateways. Billing based on “effective tokens” yielded a gross profit margin 18 percentage points higher than traditional cloud hosting services.

Leap 2: MLaaS → DaaS (Data-as-a-Service)

AIDC operators transformed desensitized industry logs, images, and voice data into “data crude oil”. Customers could purchase ready-made datasets to train small models, eliminating the triple costs of data collection, annotation, and compliance. In medical imaging, for example, China faced a 12 PB shortfall in compliant data in 2025. AIDCs aggregated data from 300 hospitals into a “white-box data lake” using federated learning and privacy-preserving computing, with a single medical image data point priced at 0.8 yuan and a gross profit margin of 55%.

Leap 3: DaaS → Outcome-as-a-Service

More aggressive operators entered into “outcome-based performance contracts” with clients: for instance, cutting scrap rates by 1% in steel mills in exchange for a 5-yuan per ton revenue share; or reducing non-performing loan ratios by 0.5% for banks in return for a 0.1% commission on credit lines. This elevated AIDCs to the role of “AI partners” rather than mere computing power vendors.

Industry Scenario Reconstruction: AIDCs as Industrial Routers

Telecommunications – From “Traffic Pipes” to “Computing Power Networks”

Operators co-located 5G-A small cells with edge AIDCs, launching “computing power packages”: a monthly 10,000-yuan 5G private network subscription included local inference time equivalent to 1 “card-hour”, with latency < 10 ms. By 2025, 30% of the B2B revenue of China’s three major telecom operators came from “computing power value-added services” rather than traffic fees.

Manufacturing – From “Factory Informatization” to “AI-Native Factories”

AIDCs packaged quality inspection, process optimization, and energy scheduling into standardized SaaS solutions. Factories only needed to deploy a 2U edge box locally to access cloud-based large models. A leading white goods manufacturer saw a 38% reduction in copper pipe welding defects for air conditioner compressors just 6 weeks after implementation, saving 120 million yuan annually in rework costs.

Healthcare – From “Tertiary Hospital Centralization” to “Grassroots Universal Access”

Through “edge AIDCs + 5G remote ultrasound”, county-level hospitals could real-time access 70B-parameter multimodal models in the cloud to automatically generate imaging reports. In 2025, the average misdiagnosis rate in medical imaging across 1,200 counties in China dropped by 2.3 percentage points, equivalent to reducing 41,000 medical disputes annually.

Finance – From “Post-Hoc Risk Control” to “Generative Compliance”

After deploying local AIDCs, securities firms used large models to real-time monitor traders’ chat records and generate “compliance scripts”, shifting from post-audit to pre-emptive risk interception. In 2025, a top-tier securities firm saw its regulatory rating upgraded by two levels thanks to AI compliance, boosting its financing capacity by 6 billion yuan.

Industrial Restructuring: The Emergence of a Four-Tier New Ecosystem

Compute BuildersThey are responsible for civil engineering, energy supply, and electromechanical systems. Their revenue model shifted from “selling data center space” to “selling kilowatts”. They offer 10-year contracts guaranteeing PUE, WUE, and CUE (Carbon Usage Effectiveness), with penalty clauses for non-compliance.

AI OrchestratorsThey provide full-stack software covering bare-metal infrastructure, Kubernetes, and large model scheduling. They aggregate diverse computing power from upstream providers and expose a unified API to downstream users, charging a 6%–8% commission based on effective computing power usage.

Data RefinersSpecializing in data cleaning, annotation, synthesis, and compliance, they transform data into tradable assets using federated learning and blockchain-based data ownership verification, capturing premium value from “data refining”.

Outcome IntegratorsClosely aligned with clients’ business needs, they sign outcome-based contracts as “AI partners”. Their core competencies include industry expertise, large model fine-tuning, and operational support, with gross profit margins reaching up to 40%.

The Double-Edged Sword of Regulation and Ethics

Energy Consumption Red Lines

China’s “East Data West Computing” project mandated that newly built AIDCs in 2025 source no less than 65% of their energy from renewable sources and maintain a PUE below 1.15, failing which energy usage permits would not be issued. This spurred the emergence of green power futures exchanges in regions like Inner Mongolia and Guizhou, allowing AIDC operators to lock in wind and solar energy prices 3 years in advance.

Cross-Border Data Flows

The EU’s AI Act came into full effect in 2025. Models with computing power exceeding 10²⁵ FLOPs were classified as posing “systemic risks”, requiring the deployment of independent AIDCs within the EU and annual audits. Chinese cloud service providers were forced to build “sovereign AI clouds” in Frankfurt and Dubai, with investments exceeding 6 billion US dollars.

Algorithmic Bias

A 2025 ruling by the U.S. Equal Employment Opportunity Commission (EEOC) stipulated that if AI recruitment models produced “disparate impacts” on minority groups, companies must disclose the sources of their training data. AIDC operators were compelled to provide “explainability reports”, standardizing model traceability and data lineage as mandatory deliverables, otherwise clients faced substantial financial penalties.

Future Outlook: What Will AIDCs Look Like in 2030?

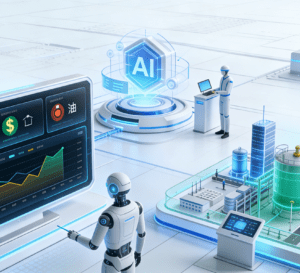

Computing Power as CurrencyGlobal “computing power exchanges” will emerge, pricing assets in FLOPs, which will rank alongside the U.S. dollar and oil as major commodities. Central bank digital currency policies will include “computing power reserves” on their balance sheets, establishing AIDCs as new “digital gold warehouses”.

Zero Carbon as ProfitabilityWaste heat from liquid cooling systems will be integrated into urban heating networks through regional pipelines, turning AIDC operators into “green utility companies”. Carbon credits will be listed on exchanges, with 25% of EBITDA derived from carbon asset monetization.

Quantum-Classical HybridizationBy 2028, the cost of quantum error correction will drop below 1 US dollar per kilqubit. AIDCs will incorporate a “quantum acceleration layer” for large model Monte Carlo sampling and combinatorial optimization, cutting training time by another 30%.

Autonomous Operations and MaintenanceAI digital employees will provide 24/7 monitoring with a fault prediction accuracy rate exceeding 99.5%. On-site maintenance staff will be reduced by 80%, making unmanned, fully dark data centers the norm, with inspections conducted solely by robots and drones.

Conclusion

In 2025, AI data centers achieved the ability to “self-evolve” for the first time: technically, they completed the leap from air cooling to liquid cooling, from CPU-centric to GPU-centric architecture, and from standalone machines to computing clusters. Commercially, they broke free from the old model of cabinet rental to directly share in industrial profits. From a regulatory perspective, they moved from passive compliance to proactively designing new standards for “green, secure, and explainable” operations. It is foreseeable that AIDCs will no longer be a “supporting link” in the IT industry chain but will become the “central intelligent core” of the digital economy. They will package computing power, data, algorithms, energy, carbon assets, and industry knowledge into globally tradable “new commodities”, thereby redefining “what a company is, what an industry is, and what constitutes infrastructure”. In the timeline of 2025, AI data centers are not only the largest testbed for technological revolution but also the new starting point for the next round of global economic restructuring.